CCU/CCS as business opportunity

In its “Green Deal”, the European Union pledged to become carbon neutral by 2050. As we speak, negotiations in the European Parliament and the Council are in full swing on the European Commission’s proposals for the “Fit for 55” package which aims to reduce greenhouse gas emissions by 55% by 2030.

Soon after the publication of the Green Deal, Cembureau, the European Cement Association, set out its ambition to reach carbon neutrality by 2050 over the cement-concrete value chain with intermediate gross CO2 reduction targets of 30% over cement and 40% over the cement-concrete value chain by 2030.

In order to achieve these targets, the cement industry focuses on a combination of innovation, technology and improved business processes in both cement manufacturing and concrete applications with an emphasis on increased alternative fuel use and the search for low carbon cements and concrete.

As the decarbonisation of limestone through calcination causes 60%-65% of cement manufacturing emissions (process emissions as opposed to combustion emissions from fuels used to heat the kiln), a successful decarbonisation of the cement industry hinges on tackling these process emissions.

That is where carbon capture and storage/use play an essential role: according to the Cembureau Roadmap, the use of different carbon capture techniques will reduce CO2 emissions by 42% by 2050.

Projects are under way

Cement companies are announcing a series of carbon capture projects whereby different capture technologies are explored, including post-combustion, oxyfuel and direct separation technologies. Trials are underway to find ways of concentrating the CO2 in the gas stream in order to make carbon capture more efficient and cost-effective.

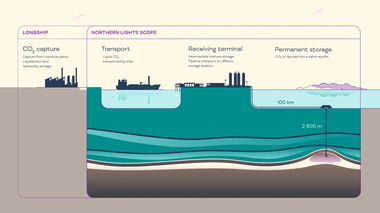

Captured CO2 can then be transported to geological formation (e.g. empty gas fields) where it is permanently stored. Other permanent storage options include the use of recycled concrete aggregates and minerals. Algae can also be used to absorb CO2 and grow biomass which can be used to fuel the kiln. Captured CO2 can also be used to create synthetic fuels such as for aviation purposes.

Many of the projects are in pilot or demonstration phase. The Cembureau Roadmap does not foresee commercial scale-up before 2030 but the roll-out and full potential for carbon capture and storage/use projects needs to be reached between 2030 and 2050.

A Facilitating regulatory framework

A healthy business case for carbon capture and storage/use requires a correct regulatory and financial framework to be put in place. The three main building blocks for such framework are:

Public financing: carbon capture technologies are breakthrough endeavours that carry a technical and a financial risk. Therefore, it is crucial that public financing opportunities are available in a transparent and accessible manner. Cembureau is pleased to see a strong focus in the “Fit for 55” package on innovation funding but stresses the importance of a close coordination with other funding instruments along the “technical readiness levels “(TRL’s) as well as with funding support offered by Member States in the form of state aid. The role of state aid scrutiny and policy will also be essential in assessing new financing instruments such as the “Contracts for Difference” that have received attention in the Commission’s impact assessment accompanying the “Fit for 55” package.

CO2 infrastructure: capturing the CO2 does not in itself lead to a CO2 reduction; it is crucial to ensure the CO2 can be transported and permanently stored; investment in CO2 pipelines and storage sites is a prerequisite for the successful deployment of carbon capture projects. As this type of infrastructure will not only serve the cement sector but all energy-intensive sectors with process-related emissions, the establishment of the infrastructure is a typical example of a public-private partnership where industry develops the capture technology and, through a joined-up approach, national and EU authorities take the responsibility for the financing of the infrastructure as well as for the permitting and public acceptance issues related to it.

Proper accounting rules for use: apart from permanently storing the CO2, which can be dine in storage sites or through mineralization in construction products, CO2 can be used in other applications such as synthetic fuels. However, an industrial site operator or its mother company will not invest in a capture project if it cannot deduct the CO2 emissions captured from its original manufacturing emissions. While the current legislation allows such deduction for permanent geological storage and for CO2 chemically bound in products, it is not clear when it comes to CO2 which is transferred to a third operator and is ultimately released into the atmosphere. The question on who will account for the CO2 released is a crucial one to determine the financial viability of capture projects by industrial manufacturers.